Monetary policy and the market-based R-star

KEY POINTS

An interest rate which cannot be observed

Conceptually, we can decompose the yield on a risk-free bond into four parts - the natural interest rate (aka ‘r-star’), monetary policy anticipation, expected inflation and risk premiums. However, the interplay between markets and central banks on the topic of the so-called ‘r-star’ – and its effect on monetary policy’s stance, bond yields and risk premia - is an intricate one.

In 2002 economists Thomas Laubach and now-New York Federal Reserve (Fed) President John Williams defined the modern view of r-star as “the real short-term interest rate consistent with output converging to potential, where potential is the level of output consistent with stable inflation”.

More simply, it is often referred to as the short-term interest rate which would prevail when the economy is at full strength and inflation is stable.

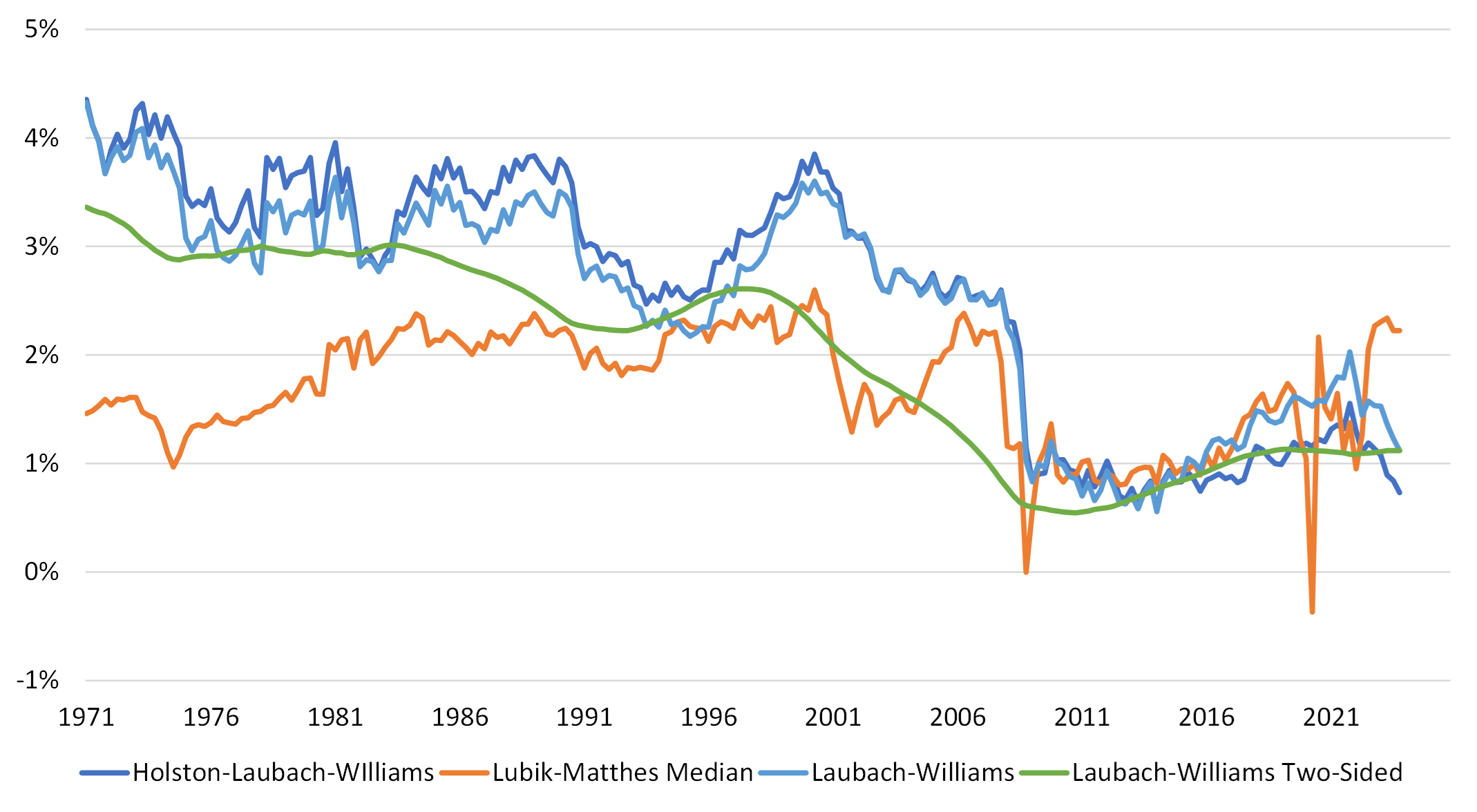

Figure 1: US natural rate of interest estimates

Source: Bloomberg

The Fed publishes several estimates of r-star - see Figure 1. Note the wide dispersion in most recent estimates, from 0.75% to 3.1%. A similar range can be observed in Eurozone estimates which were recently published by the European Central Bank. Also, note r-star’s dynamic nature, averaging 2.5% from 1970 to 2002 before dropping to as low as 0%-0.5% in 2009 and to a similar level in the aftermath of the pandemic shock.

The yield curve comes to the rescue

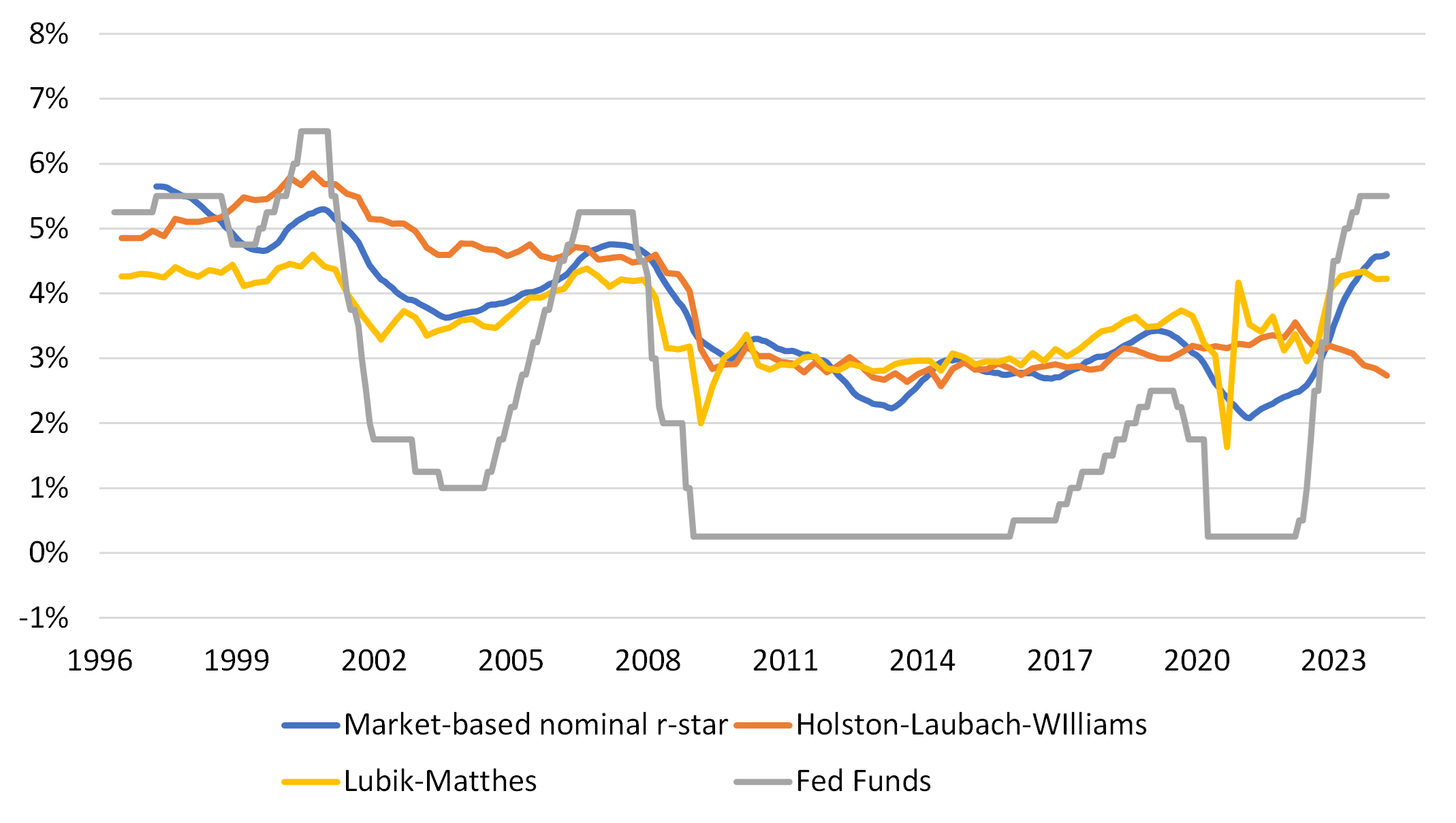

Luckily for financial markets practitioners, yield curves are an invaluable source of information as they immediately discount complex scenarios at any forward date. For example, the forward interest rate market allows us to construct a market-based estimate of the r-star. The implied one-month interest rate in five-years’ time gives us an approximation of the future equilibrium policy interest rate expected by market participants. Adjusting this by subtracting an estimate of the term premium (the additional return required on lending for longer periods) gives us an estimate of the nominal r-star rate.(See Figure 2).

Figure 2: Model and market-based r-star

Source: AXA IM, Bloomberg

Four aspects are worthy of note:

- There is a substantial 140 basis points (bp) gap between model-based estimates. While this is entirely due to different statistical methodologies, it does highlight the level of uncertainty about the true value of this metric

- Our market-based r-star measure seems to better reflect the Lubik-Matthes estimate

- At around 4.5%, our market-based r-star is now 170bp above the 2009-2019 average level.

- It’s not clear how monetary policy and hence market-based r-star measures ultimately influence the true but unobservable level of r-star. Economist Gianluca Benigno (2024)

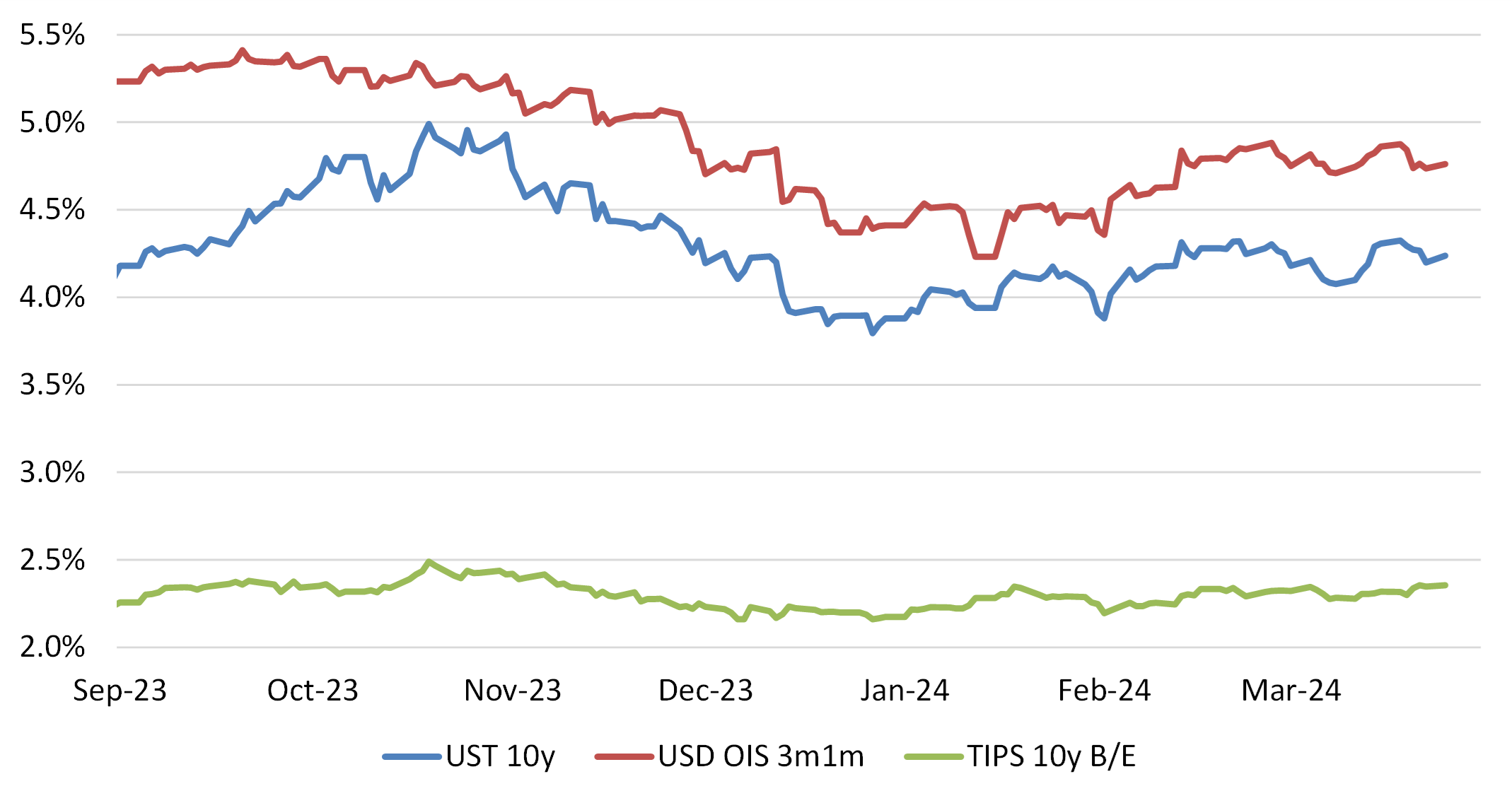

Figure 3: Factors affecting US Treasury yields

Source: Bloomberg

Policy uncertainty = Higher risk premium

The high level of uncertainty around r-star automatically translates into uncertainty about the monetary policy stance. Again, we can refer to an example from the Fed’s past, when measurement errors did ultimately bias its perception to the point of erroneously calibrating monetary policy at the end of the 1960s. The high and volatile inflation during the 1970s might have been partially avoided “if the Federal Reserve had possessed excellent information regarding the structure of the economy”.

The parallel with today’s markets can be easily drawn - what if the natural interest rate was higher than current estimates? What if the long-run dot (r-star) at 2.6% failed to capture the changing structure of the economy? Evidently, the actual monetary policy stance would not be as tight as is widely believed, in which case risk premia across asset classes are probably too compressed to compensate investors for a scenario of repricing of a new interest rate regime.

In practical terms, it is likely the current level of the Fed Funds Rate is above most estimates of the r-star. Hence, policy is restrictive and inflation appears to be heading lower. This justifies market expectation of some easing of policy in the year ahead. However, the message from central bankers – perhaps reflecting their own internal discussions about the neutral rate – is that markets need to be careful about pricing in too many rate cuts. This in turn has implications for expected returns across bond markets and is a strong support for short-duration strategies in fixed income, given that yields curves are inverted and thus pricing in much lower rates in the future.

Aggiornati sui mercati in modo veloce, ma approfondito

Partecipa al webinar in diretta con Alessandro Tentori, CIO Europe AXA IM, ogni martedì alle 11.00

ISCRIVITIDisclaimer

AXA IM e BNP Paribas Asset Management stanno progressivamente fondendo e semplificando le loro entità legali per creare una struttura unificata. AXA Investment Managers è entrata a far parte del Gruppo BNP Paribas nel luglio 2025. A seguito della fusione di AXA Investment Managers Paris e BNP Paribas Asset Management Europe e delle rispettive holding, avvenuta il 31 dicembre 2025, le società combinate operano ora sotto il marchio BNP Paribas Asset Management Europe.

Prima dell’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di BNP Paribas Asset Management. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta, anche fuori sede, o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di BNP Paribas Asset Management o di società ad essa affiliate. L’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché BNP Paribas Asset Management impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. BNP Paribas Asset Management declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

BNP Paribas Asset Management non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di BNP Paribas Asset Management delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di BNP Paribas Asset Management e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

BNP Paribas Asset Management può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

BNP Paribas Asset Management si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

Redatto da BNP Paribas Asset Management Europe. © BNP Paribas Asset Management 2026. Tutti i diritti riservati.