China Outlook – Short-term reprieve, long-term challenges

- 01 Dicembre 2023 (5 min di lettura)

Key points

- 2023 – the first-year post-pandemic – endured a sluggish first half due to wavering confidence and delayed policy boosts. Stimulus has quickened the pace since

- 2024 is expected to grow at a faster quarterly pace, backed by supportive measures and eventually firmer external demand

- But the economic upswing from announced stimuli looks set to fade into 2025 and could lead to future imbalances, requiring a potentially prolonged adjustment period

Free from COVID-19 disruptions but marked by scars

China’s harsh zero-COVID policy was lifted at the end of December 2022. 2023 was the first year without COVID-19 disruptions. However, the economic recovery faced hurdles. Despite an initial rebound in the first quarter (Q1), several headwinds emerged, exerting pressure on the economy. Somewhat delayed but solid stimulus measures have supported the economy, positioning it well to meet this year's growth target of "around 5%”.

The three-year rollercoaster of pandemic restrictions and real estate turmoil have eroded public confidence, evident in weak prices, subdued consumption and sluggish investment in the first half of the year. Beijing began acting in August, unveiling substantial policy support – particularly in mortgage easing – aimed at stimulating housing demand and alleviating household financial pressures.

The outlook for China’s economy appears to hinge critically on the central government going forwards. Should it provide adequate and timely supports to meaningfully restore consumer and investor confidence, we would anticipate a brighter 2024 and a more stable 2025.

Investment is transmission of stimulus

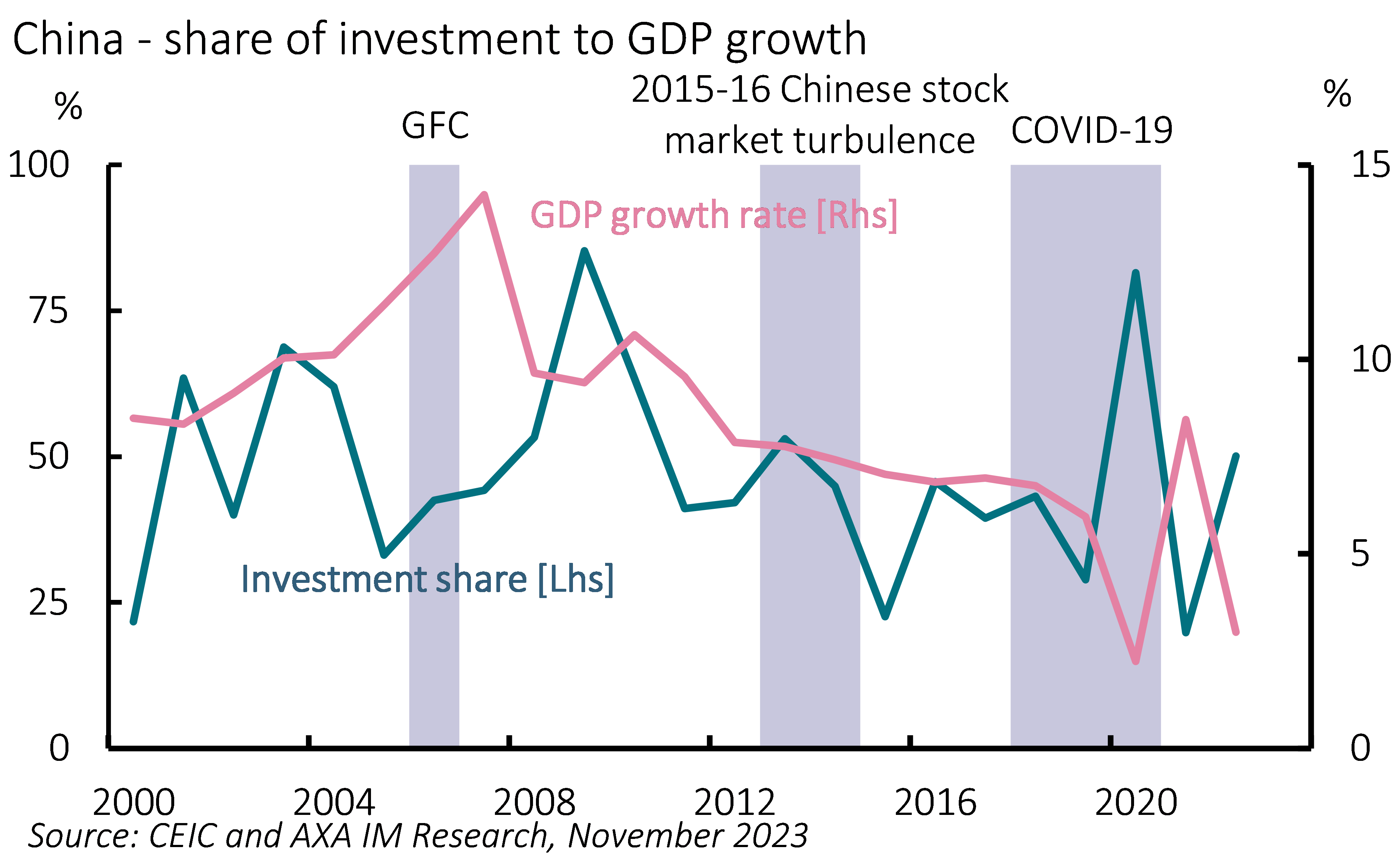

According to Beijing’s conventional economic doctrine, investment, consumption, and exports are the ‘three carriages’ driving economic growth. When the economy experiences sluggishness, stimulus-backed investment has typically become the marginal policy tool to support growth (Exhibit 1). This time has been no exception. In July, Beijing mandated the acceleration of Local Government Special Bonds issuance. In October, the unusual mid-year budget review surprised markets by adding one trillion renminbi to the budget deficit. Alongside the early issuance of next year’s quota for Local Government Bonds (LGB), these directives aim to bolster investment, providing more support as we move into 2024.

Historically, stimulating investment through LGB issuance funnels spending into infrastructure projects, which typically have extended timelines. Consequently, the impact of such stimulus is not immediate but rather gradual. We anticipate continuous investment support throughout 2024, thereby sustaining the economy.

Exhibit 1: Investment has saved GDP growth several times

Exports are to follow

This year presented formidable challenges for China’s exports, due to global inflation and reduced consumer spending in developed countries. Despite this, certain sectors like mechanical and electrical products and automobiles held up well, with China even surpassing Japan to become the world’s top auto exporter, driven by its growing electric vehicle exports since 2018.

As part of its ‘industrial upgrading’ initiative, China aims to boost high-value manufacturing in its exports. Looking ahead, as inflation eases in developed economies, global demand is expected to recover, potentially improving China’s export situation by late 2023 into 2024 and beyond. However, uncertainty looms due to geopolitical dynamics. Any stringent restrictions from the US or European Union could significantly impact China’s exports and its manufacturing sector. The recent Asia-Pacific Economic Cooperation (APEC) meeting between Presidents Joe Biden and Xi Jinping suggested a thawing in relations, with the US lifting some restrictions, including on a key China agency. However, next year’s US elections could lead to a swift reversal of this warming.

Consumption relies on the property market

China is a nation of homeowners. A 2020 study1 showed that over 80% of Chinese households own their home. Due to limited investment options in the economy and an inadequate social security system, housing is also the primary investment avenue for Chinese households. Over 20% of urban households own multiple homes, often without generating rental income. Residential property holds a significant 60% of household assets, a stark contrast to the US where it's around 30%.

Since the property market turmoil began in 2021, Chinese households have fretted over asset values, leading to muted consumption and a persistent increase in precautionary saving. This behaviour is not purely reflective of mortgage payments impacting incomes, but rather to compensate the financial insecurity resulting from property devaluation – a wealth effect. Therefore, stabilising the property market is crucial to bolster consumer confidence and underpin consumption.

Efforts have been made since August on monetary and fiscal fronts to alleviate pressure on household finances and enhance housing demand. However, addressing the structural issues in the property sector will be a long journey, which is now only at the start. Continuous government support is vital not only for housing market stability, but to prevent prolonged repercussions on related sectors like construction and private consumption.

Our base view is Beijing will implement adequate measures to support the demand side of the housing market over the coming two years, allaying concerns among households. As the services sector and labour market recover, consumer confidence should rise across 2024. Consequently, improved sentiment and reduced fluctuations in pork prices should enhance consumer prices moving forward. We expect Consumer Price Index inflation to average 1.1% in 2024, before reaching 2% in 2025.

Policy supports now risk future problems

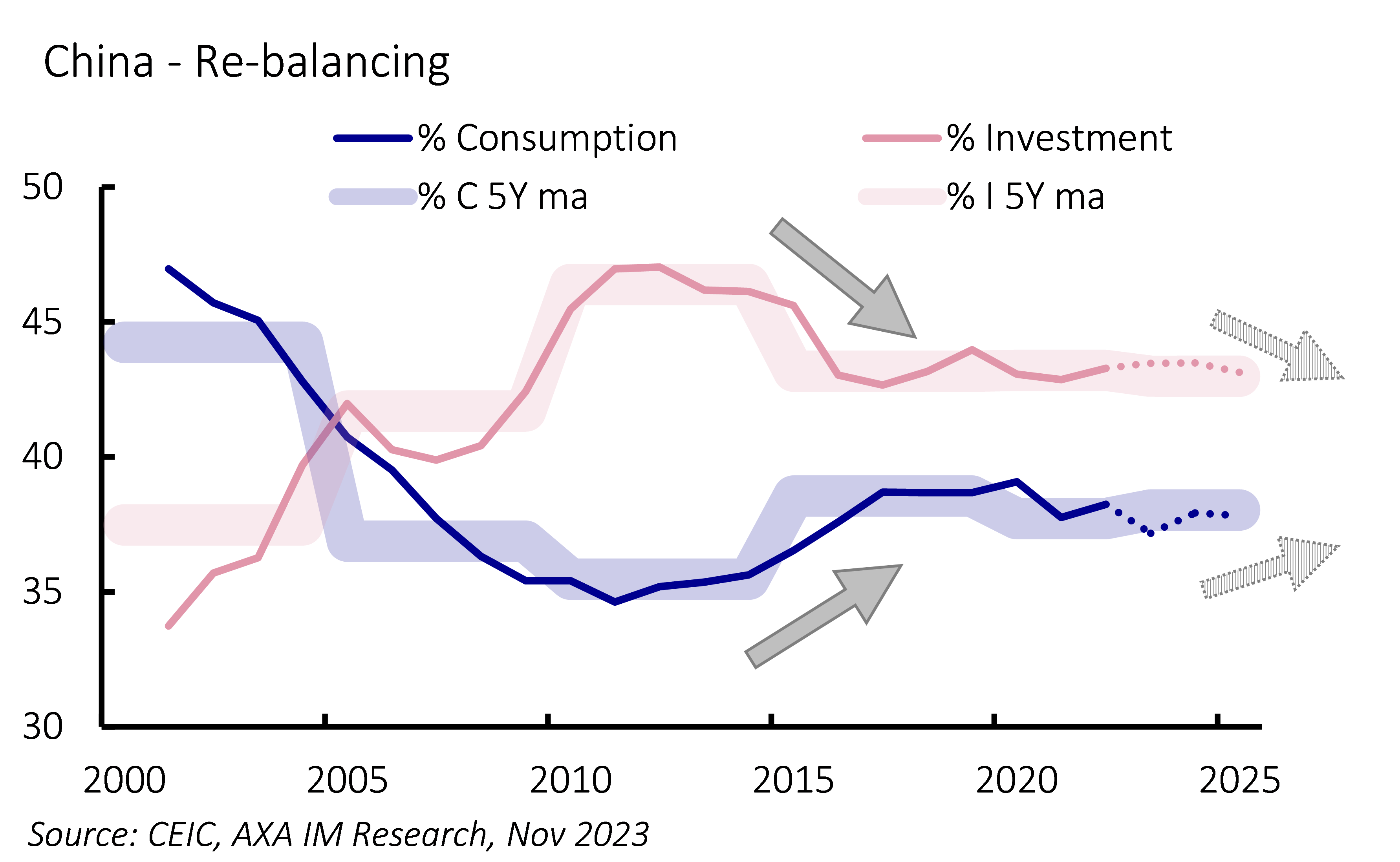

The economy requires policy backing to avert a severe downturn. However, Beijing’s strategy mirrors past investment-driven growth models. While historical data are testimony to the short-term effectiveness, it bears future costs. The bulk of local government investments inevitably funnel into infrastructure projects, which mainly provide public goods, typically yielding low returns. This situation strains local government balance sheets. Although the central government has recently indicated willingness to assume more debt on behalf of local governments, it perpetuates a cycle of ‘more debt, more investment, low return’, exacerbating resource misallocation.

Yet this investment-centric model (Exhibit 2) is Beijing's most familiar and seemingly most-favoured option. Direct fiscal stimulus to households has never been used, with no established channels for such delivery and questions over its effectiveness without a reversal in public confidence.

In 2024, China is expected to prioritise addressing the challenges posed by property market woes and local government indebtedness. Coordinating fiscal and monetary tools for economic support is likely the approach. We expect this to prompt faster quarterly growth in 2024, followed by a slowdown in 2025 as the stimulus effects wane. We estimate annual growth to peak at 4.5% in 2024 before easing to 4.2% in 2025.

Exhibit 2: When re-balancing will be back to agenda

Structural reform is the solution in the long run

The impressive ‘Chinese speed’ of economic growth over the past 40 years owes its success to several key factors: the demographic dividend; World Trade Organization accession; East Asian reshuffling; and, underpinning these, structural reform. The economic reforms of former leader Deng Xiaoping in 1978 spurred China’s current economic and global influence. Policy stimulus effectively tackles cyclical issues, providing short-term boosts, but long-standing structural issues resurface when this support wanes – a challenge acknowledged by Beijing. The critical question remains – can it relinquish its grip and embark on much-needed structural reforms? Based on President Xi’s recent behaviour, we have our doubts.

1Huang, Y., Yi, D., & Clark, W. A., “Multiple home ownership in Chinese cities: An institutional and cultural perspective”, Cities Vol.97, February 2020.

La nostra view per il 2024

Vedi tutti i contenuti

Outlook 2024: USA avanti, Europa col freno, no recessione

- A cura di

- 05 Dicembre 2023 (5 min di lettura)

Crescita globale rallenta, ma guadagni potenzialmente elevati per le obbligazioni

- A cura di ,

- 05 Dicembre 2023 (7 min di lettura)

Outlook 2024-2025 (Webinar)

- A cura di

- 05 Dicembre 2023 (15 min di lettura)

I tassi a lungo termine e l’evoluzione del debito negli Stati Uniti e in Europa

- A cura di

- 05 Dicembre 2023 (7 min di lettura)

Investment Strategy Outlook – Modest growth, modest returns

- A cura di

- 04 Dicembre 2023 (7 min di lettura)

Pensions investment outlook 2024: Mining for opportunities amid easing growth

- A cura di

- 04 Dicembre 2023 (7 min di lettura)

Disclaimer

Prima dell’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave per gli investitori (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di AXA Investment Managers. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione. Maggiori informazioni sulla politica dei reclami di AXA IM sono al seguente link: https://www.axa-im.it/avvertenze-legali/gestione-reclami. La sintesi dei diritti dell'investitore in inglese è disponibile sul sito web di AXA IM https://www.axa-im.com/important-information/summary-investor-rights.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di AXA Investment Managers o di società ad essa affiliate, né la raccomandazione di una specifica strategia d'investimento o una raccomandazione personalizzata all'acquisto o alla vendita di titoli. L’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché AXA Investment Managers impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. AXA Investment Managers declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

AXA Investment Managers non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di AXA Investment Managers delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di AXA Investment Managers e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

AXA Investment Managers può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

AXA Investment Managers si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

A cura di AXA IM Paris – Sede Secondaria Italiana, Corso di Porta Romana, 68 - 20122 - Milano, sito internet www.axa-im.it.

© 2024 AXA Investment Managers. Tutti i diritti riservati.