Market Outlook - Fixed income: Monetary policy should bolster markets

KEY POINTS

Fixed income markets should benefit from continued central bank easing in 2026. We expect lower interest rates in the US as policymakers respond to weaker labour market trends, and lower rates in Europe because of further declines in inflation. A resilient global economy and policy measures should keep fiscal concerns in check, allowing yields across the curve to reflect the growth and inflation outlook. The core scenario is positive for credit markets notwithstanding tight credit spreads and signs of increased leverage.

Central bank policy, as always, remains key to the bond market outlook in 2026. Major central banks are forecast to take short-term interest rates to or below estimated neutral levels in response to growth risks and falling inflation expectations. The International Monetary Fund’s recent growth forecasts were better than those made earlier in 2025 but still suggest advanced economies will struggle to meet long-term average growth rates in the years ahead.

That implies a more supportive stance from central banks as long as inflation remains close to targets. For next year, this suggests substantial reductions in US interest rates to below 3%. Additional US Treasury market yield curve steepening is likely to result. However, demand for yield remains strong, not least from the US insurance sector which has become a significant source of structural demand. Long-term yields are unlikely to significantly deviate from the trading range established in 2025.

Europe’s potential

The European Central Bank lowered its deposit rate to 2.0% in June 20251. Further cuts are possible should inflation undershoot the official target. This limits the potential for higher yields in European government bonds. However, once Germany’s ambitious spending programme gets underway there will be more supply of debt in the Eurozone’s biggest bond market, which could pressure markets at times. A steeper rate curve in the Eurozone is likely.

Outside of the bloc, the UK offers potential for attractive returns as markets only expect limited Bank of England easing. Lower inflation and tighter fiscal policy should drive UK gilt yields lower in 2026.

Despite this benign rate outlook, sovereign markets will remain at risk of increased investor concern on the fiscal side. The last year has seen government bond yields rise relative to equivalent maturity interest rate swap rates – a sign of increased risk premiums. Despite rate cuts, long-term yields have moved higher than their end-2024 levels.

The long-term trend for government debt levels is not encouraging in advanced economies, posing further scope for risk premiums to rise. However, the benign outlook for nominal growth and government attempts to take policy steps to appease bond market investors should limit any cases of ‘fiscal panic’. Steeper yield curves will at least offer investors potentially higher carry-driven returns in longer-duration strategies than has been the case for a while.

- European Central Bank, Key ECB interest rates, November 2025

Credit bounce

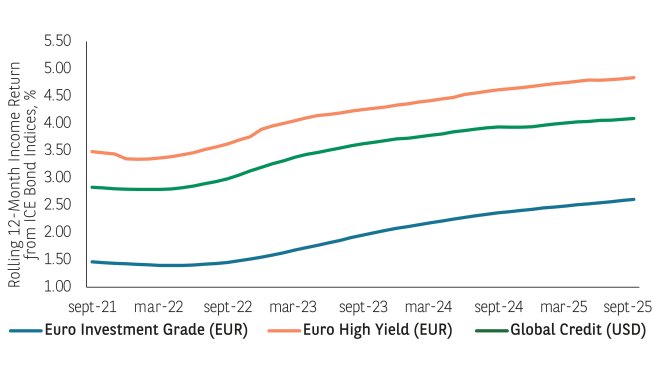

Credit market activity has remained buoyant in 2025 with credit spreads narrowing over the course of the year despite elevated levels of issuance. Excess returns have been positive and underlying corporate fundamentals remain solid. Looking forward what will determine credit market performance is whether investors continue to value diversified exposure to corporate risk more highly than balance sheet-challenged sovereign debt. In which case, prevailing yields in credit markets are attractive and should deliver attractive income-driven total returns.

However, from a credit spread point of view, current valuations are tight, and the key risk is credit markets will experience periods of underperformance relative to government bonds. Catalysts for this are weaker economic data, equity market volatility or evidence of growing credit stresses in either private or public markets.

Geographically, US markets are most at risk from any deviation from the benign core scenario. Tariffs and the impact of immigration controls on labour supply could combine to keep inflation higher for longer. This not only complicates the Federal Reserve’s decision-making but also reduces expected real returns from US fixed income. It could also negatively impact the dollar. Any sense of increased politicisation of monetary policy (fiscal dominance) will tend to increase inflation expectations, steepening the US yield curve further and underpinning inflation break-even levels. If growth also turns out to be weaker, investors could also focus on the US fiscal outlook, again widening spreads in the US rates and credit markets.

In the absence of a growth or credit shock, carry will be a major theme for bond investors, delivering most of the total return. As such, high yield and emerging market bonds continue to be interesting from a total return perspective. Again, after a robust performance in 2025, investors need to be mindful of valuations but improved credit quality in high yield and better macroeconomic performance in emerging markets are positives for those markets. Significant drawdowns in fixed income markets tend to only occur in response to a growth or credit shock. Neither is in our core scenario for 2026 which means investors should be able to benefit from solid bond income returns.

Disclaimer

Comunicazione di marketing: Prima dell’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave per gli investitori (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di AXA Investment Managers. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione. Maggiori informazioni sulla politica dei reclami di AXA IM sono al seguente link: https://www.axa-im.it/avvertenze-legali/gestione-reclami. La sintesi dei diritti dell'investitore in inglese è disponibile sul sito web di AXA IM https://www.axa-im.com/important-information/summary-investor-rights.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di AXA Investment Managers o di società ad essa affiliate, né la raccomandazione di una specifica strategia d'investimento o una raccomandazione personalizzata all'acquisto o alla vendita di titoli. L’investimento in qualsiasi fondo gestito o promosso da AXA Investment Managers o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché AXA Investment Managers impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. AXA Investment Managers declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

AXA Investment Managers non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di AXA Investment Managers delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di AXA Investment Managers e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

AXA Investment Managers può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

AXA Investment Managers si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

A cura di AXA IM Paris – Sede Secondaria Italiana, Corso di Porta Romana, 68 - 20122 - Milano, sito internet www.axa-im.it.

© 2025 AXA Investment Managers. Tutti i diritti riservati.