The long view

Go through the thought process. Imagine setting out a 20-year asset allocation plan today. Stocks are at all-time price and valuation highs, bonds are closer to fair value, but credit spreads are super tight. Not easy, is it? Is the traditional mechanistic flightpath asset allocation appropriate for where we are? There are lots of risks potentially materialising. History suggests valuations are a concern for equities, especially in the US. Bonds, however, are set to potentially generate long-term gains close to current yield levels, consistent with average nominal GDP growth. Time is the friend of the long-term view, as should be discipline, rebalancing and compounding. Done correctly, history suggests a 10% compound annual return over a decent horizon is the reward for patience and planning.

- I still like credit in fixed income; it appears solid and demand is strong

- I am concerned about the disconnect between macroeconomic and political risks and markets

What will it take?

In several client meetings recently, the issue of what might burst the ‘risk-on’ bubble has been discussed. I think this reflects a general level of discomfort between perceived threats to the global outlook and markets’ remarkably strong performance. The US narrative continues to add to uncertainty, with the investment thesis around some climate change solutions and selected pharmaceutical products being challenged most recently. The gathering of world leaders at the United Nations General Assembly in New York highlighted the changed world of international relationships and the apparent difficulties in achieving peaceful solutions in Ukraine and Gaza. Leaders gathered against a backdrop of the world trading system being upended by the preference of the US for its own tariff-led approach rather than that of the multi-lateral framework embodied in the mission of the (now less effective) World Trade Organization. At the same time, risky assets are at extreme valuations, there are concerns about inflation, US Federal Reserve (Fed) independence, fiscal stability and a potential US recession. Yet markets appear to be complacent.

Quick or slow?

Picking a single event that would cause a market correction is difficult. Think about Liberation Day in April. What the White House announced should have elicited a negative market reaction. It did, but it didn’t persist because the implementation of tariffs was postponed. There are numerous individual risks to market sentiment – higher US inflation; a monetary policy mistake; a negative bond reaction to fiscal developments in the UK or France; and an escalation of security tensions in the east of Europe. We can’t trade on any one of these risks materialising - or having a long-term impact on valuations. The fact that the VIX index and corporate bond credit default swaps remain low suggests that investors have no appetite for hedging against any of the myriad risks materialising into realistic market drawdowns.

For what it’s worth, my bet is that if there is a market correction, it will be a more drawn-out affair. The US economy is slowing, at least outside of the artificial intelligence (AI) economy, and inflation will be running at an elevated rate for some time as tariff costs are increasingly passed on to consumer prices or reduce profit margins. Meanwhile there are deflationary forces elsewhere in the world. Somehow, it does not seem likely that nominal GDP growth can remain as robust as it has. All G7 countries, except for Japan, had a much lower year-on-year nominal GDP growth rate in the second quarter (Q2) than the average of the previous eight quarters. That has implications for corporate earnings growth and risk premiums.

Long-term expectations

For those that entertain themselves by checking in on LinkedIn on a regular basis, you might have come across posts of charts that show the relationship between market prices (valuations) and subsequent future returns. The most popular suggests current US equity market valuations would – if history is any guide – be consistent with annualised total returns of close to zero over the next 10 years. Using current versus subsequent changes in the price-to-earnings (P/E) ratio alludes to a similar outcome. When the P/E ratio has been near to today’s level in the past, the subsequent five to 10 years have seen between a five-to-10-point decline in the multiple. A 10-point decline in the P/E multiple over the next decade would require annual earnings per share for the S&P 500 to grow by a compound 16% if a 10% return from the market each year was to be maintained. That is asking a lot of AI-related earnings growth.

Of course, history does not guarantee future outcomes. However, there has never been 16% earnings growth over such a sustained period. The risk is the modest deterioration in US GDP growth and inflation extends to more of an economic malaise over time, undercutting risk valuations and returns.

Planning

It’s important for long-term investment strategies to have a view on what total returns might be over the medium term. Target retirement date strategies have become very popular in the US and the UK. These typically have an extended investment horizon, start with a high allocation to equities and gradually derisk as the strategy matures. They are based on the normative assumption that bonds are less volatile than stocks, and provide some diversification, and that as people near retirement they value stable income over uncertain growth. The problem is that recent experience has not been great. Bonds became very expensive in the decade after the global financial crisis, and the re-rating of bonds after 2021 destroyed performance. Savers would have been better served staying in equities since 2000 – the drawdowns in equities after the pandemic and the rates shock of 2021 were soon wiped out, while some bond positions remain underwater.

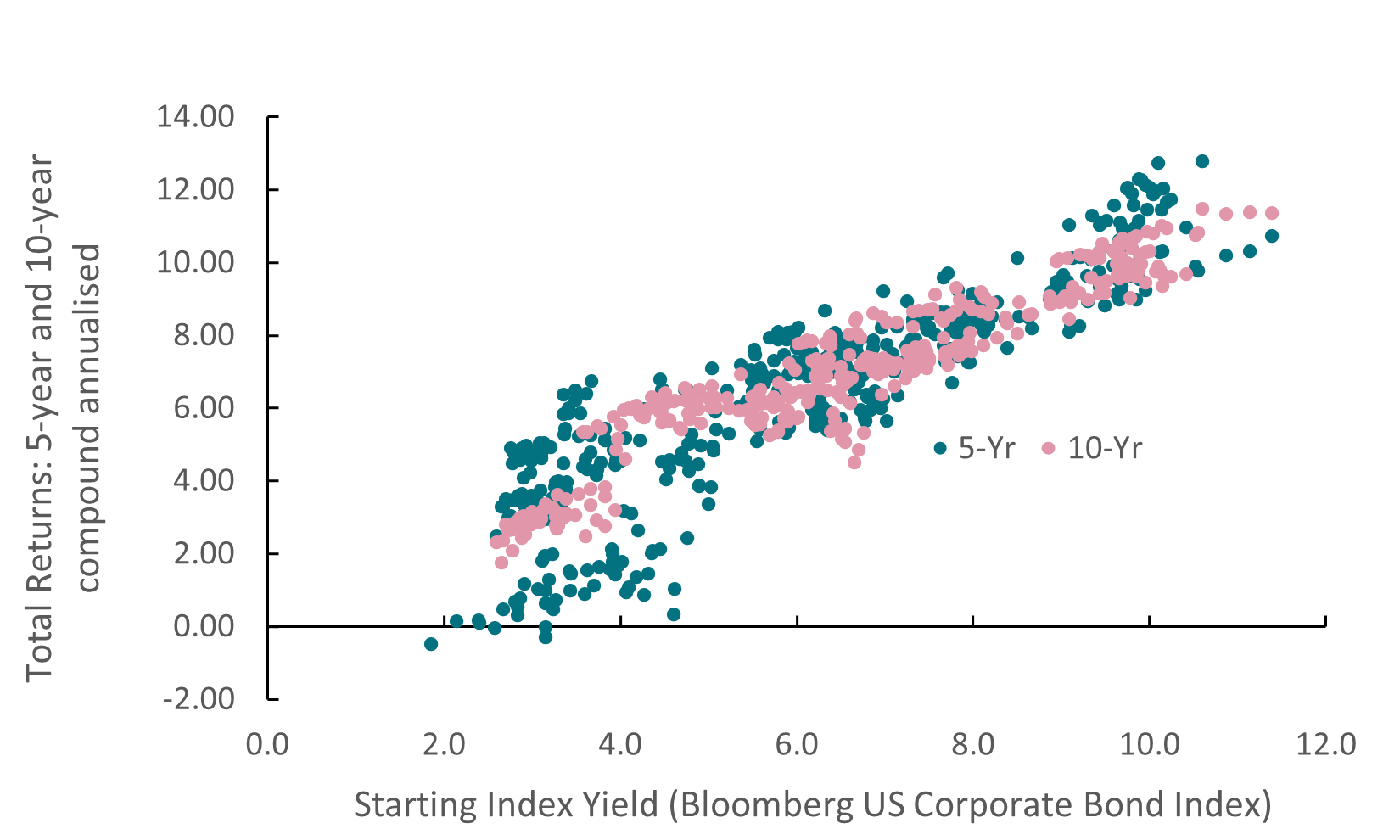

US Corporate Bond Index Returns

Source: ICE Bond Indices; Bloomberg – 25 September 2025

Different glidepath

The good news is that bonds are better value today. Doing the same valuation versus performance analysis, US government bonds - given where yields are today - should tend towards total annualised returns of 4.25% to 4.75% depending on the holding period (based on the regression of all maturity US Treasury yield and subsequent total return performance from a representative index). The data suggests, for US dollar investors, a much more balanced equity-bond allocation. High quality corporate bonds would give a little bit more fixed income performance. Sure, there are inflation and fiscal risks that can create mark-to-market volatility, but I am talking long-term investment strategies here and government bonds and high-grade corporate bonds are extremely likely to remain money good over such time periods. The traditional retirement glidepath might need to have a different starting point given the risks to equity returns from today’s valuations.

For European investors, the balance is in favour of equities over fixed income – a potential 7%-to-8% total return from stocks relative to 2% to 3% from bonds. A more positive view on European equity returns might also incorporate the potential for potential growth to improve if plans to invest in innovation, leverage progress on net zero, and increase spending on defence and infrastructure come to pass. Meanwhile, the frenzy of AI-related spending in the US might diminish at some point.

Ifs and tokens

All of this rests on economic and policy developments. Something must happen to break the US equity market to get multiples down to more sustainable levels. Something must happen to boost European growth. Inflation could again undermine returns from bonds. Moreover, passive allocations over a 30-to-40-year period might not be the most appropriate way to manage one’s retirement. A glidepath approach with decent diversification and some flexibility to change allocations based on contemporaneous valuations and macro developments could be a more fruitful approach. In time, this will also become more cost-effective as mass-market retail retirement investment products utilise technology such as the blockchain to give much cheaper access to underlying market developments. An AI-driven dynamic allocation of exposure to various bond and equity markets through cheap, easy-to-trade tokenised investments could well be the core of the asset management industry of the future.

Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, AXA IM, as of 25 September 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

AXA IM e BNP Paribas Asset Management stanno progressivamente fondendo e semplificando le loro entità legali per creare una struttura unificata. AXA Investment Managers è entrata a far parte del Gruppo BNP Paribas nel luglio 2025. A seguito della fusione di AXA Investment Managers Paris e BNP Paribas Asset Management Europe e delle rispettive holding, avvenuta il 31 dicembre 2025, le società combinate operano ora sotto il marchio BNP Paribas Asset Management Europe.

Prima dell’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di BNP Paribas Asset Management. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta, anche fuori sede, o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di BNP Paribas Asset Management o di società ad essa affiliate. L’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché BNP Paribas Asset Management impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. BNP Paribas Asset Management declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

BNP Paribas Asset Management non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di BNP Paribas Asset Management delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di BNP Paribas Asset Management e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

BNP Paribas Asset Management può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

BNP Paribas Asset Management si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

Redatto da BNP Paribas Asset Management Europe. © BNP Paribas Asset Management 2026. Tutti i diritti riservati.