Credit or Duration?

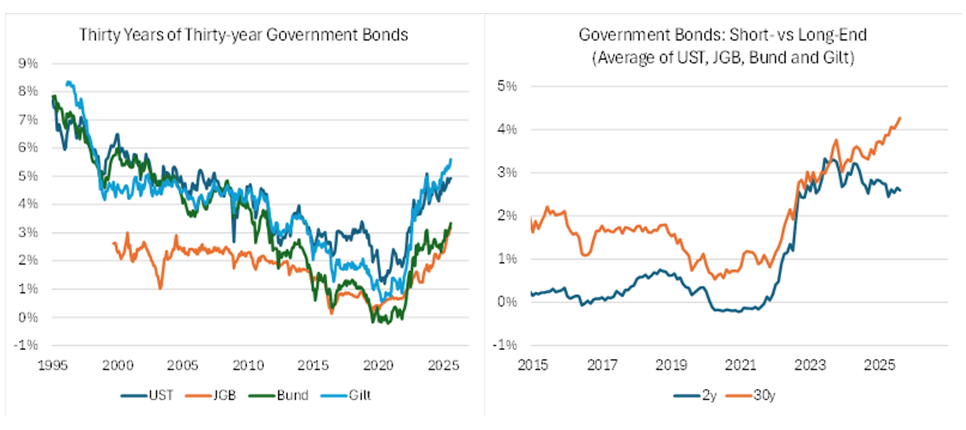

We analyse the relationship between interest rate sensitivity and credit sensitivity in fixed income portfolios with the help of a basic equilibrium approach. The post-pandemic increase in long-dated government bond yields, reflecting question marks about the state of public balance sheets as well as worries about the long-term outlook for inflation, has recently captured the attention of bond investors. At the same time, credit spreads are close to historical lows and corporate balance sheets do not (yet) appear to be affected by rising refinancing costs.

The choice. Imagine a risk-averse investor rolling an overnight risk-free position indefinitely. Basically, she has two ways to add risk and to boost her bond portfolio returns: She can either extend the duration of her risk-free cash flow or she can allocate away from the risk-free yield curve and assume credit risk. In both cases, we're dealing with spreads.

We can have a debate about the usefulness of the concept of equilibrium in social science, but in any case, it might be convenient to assume there is a point in the decision process described above, where the investor is indifferent between credit risk and duration risk, i.e.

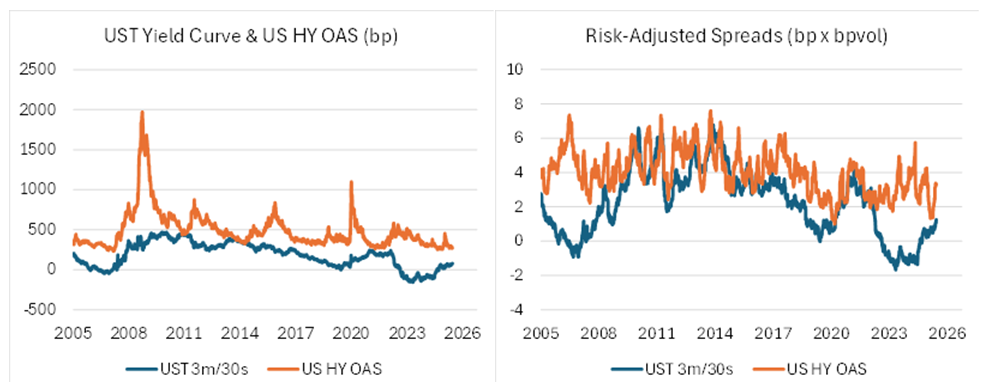

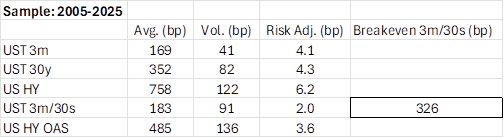

The data. Let's turn to numbers to assess the yield curve level that must be reached for the investor to be indifferent between duration and credit. Over the past 20 years, the 3-month / 30-year spread on the US Treasury curve has averaged 183bp with a volatility of about 90bp. During the same period, the US High Yield OAS has averaged 485bp with a volatility of 136bp. Hence, the indifference level on the US Treasury yield curve is approximately 325bp (“breakeven 3m/30s” in the table below). A flatter curve makes yield-enhancing credit strategies more valuable, while a steeper government bond curve makes duration-extension strategies more valuable.

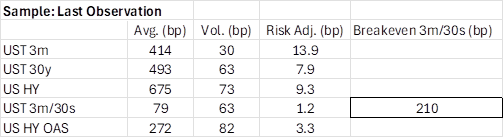

Based on the latest observation (end of August 2025), we'd have a slightly different picture: The Treasury curve is worth 79bp with a vol of 63bp. On the other hand, the US High Yield index is worth 272bp with a vol of 82bp. This results in a curve break-even of 210bp. All else equal, the US Treasury curve must steepen at least to its long-term average level of 180/200bp before an investor turns indifferent between duration and credit.

Concluding remarks. The analysis above does not consider other key aspects of the investment process, e.g. instrument liquidity and various balance-sheet related valuation adjustments (generally referred to as xVA). Considering these additional variables would provide us with a more precise idea of the equilibrium point between credit and duration, albeit at the cost of increased complexity. Keeping the analytics at a basic level, we conclude that the government yield curve might still be too flat relative to credit spreads. This result confirms investors' strong appetite for credit risk.

References

- Arrow / Debreu (1954), Existence of an Equilibrium for a Competitive Economy, Econometrica, vol. 22

- Chatterjee (2015), Modelling Credit Risk, Bank of England

- Gregory (2015), The xVA Challenge, Wiley Finance

- Joseph (2013), Advanced Credit Risk, Wiley Finance

- Litterman (2003), Modern Investment Management – An Equilibrium Approach, Wiley Finance

- Merton (1974), On the Pricing of Corporate Debt: The Risk Structure of Interest Rates, The Journal of Finance, vol. 29

- Nilson (1957), On the Notion of Equilibrium in Social Science, Acta Sociologica, vol.

- Tentori (2025), Why is the Yield Curve Soo Flat?, AXA IM CIO Quick View

- Tentori (2025), Credit or Duration? An Equilibrium Approach, AT Economics & Markets

Aggiornati sui mercati in modo veloce, ma approfondito

Partecipa al webinar in diretta con Alessandro Tentori, CIO Europe AXA IM, ogni martedì alle 11.00

ISCRIVITIDisclaimer

AXA IM e BNP Paribas Asset Management stanno progressivamente fondendo e semplificando le loro entità legali per creare una struttura unificata. AXA Investment Managers è entrata a far parte del Gruppo BNP Paribas nel luglio 2025. A seguito della fusione di AXA Investment Managers Paris e BNP Paribas Asset Management Europe e delle rispettive holding, avvenuta il 31 dicembre 2025, le società combinate operano ora sotto il marchio BNP Paribas Asset Management Europe.

Prima dell’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di BNP Paribas Asset Management. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta, anche fuori sede, o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di BNP Paribas Asset Management o di società ad essa affiliate. L’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché BNP Paribas Asset Management impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. BNP Paribas Asset Management declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

BNP Paribas Asset Management non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di BNP Paribas Asset Management delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di BNP Paribas Asset Management e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

BNP Paribas Asset Management può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

BNP Paribas Asset Management si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

Redatto da BNP Paribas Asset Management Europe. © BNP Paribas Asset Management 2026. Tutti i diritti riservati.