CIO Views: Markets hold up against volatility spike

KEY INVESTMENT THEMES

Chris Iggo, CIO AXA IM Core

August bounce may augur well for rest of 2024

Whatever triggered early August’s volatility spike has not proved serious enough to derail markets’ robust year-to-date performance. Equity and credit markets rebounded quickly while risk indicators – such as the VIX – swiftly reverted to their more benign lower levels. However, the early August moves highlighted that markets are priced to perfection and therefore, vulnerable to adverse fundamental news, even if the volatility was exaggerated by seasonally thin markets. Additional bouts cannot be ruled out in the months ahead given market sensitivity to US labour market data, Japanese monetary policy, and technology company earnings. At the same time, the rapid reversal in the risk sell-off can be seen as good news.

Fundamentals remain supportive. The Federal Reserve should start its interest rate cutting cycle soon - following the moves from other central banks. Elsewhere refinancing problems remain absent in public credit markets while second quarter corporate earnings largely met growth expectations. There has arguably been a moderation in political risk. Strong returns from risk assets might be sustained into the end of 2024, with growth equities and higher beta credit leading the way as they have for the whole of the year. High yield and other short-duration fixed income credit strategies most likely offer the lowest risk path to sustaining positive returns in the final semester of the year.

Alessandro Tentori, CIO Europe

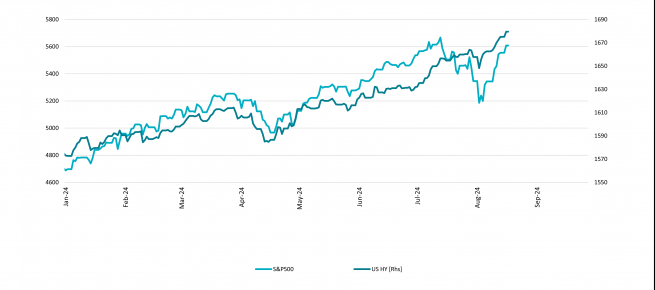

High yield’s optionality opportunity

High-yield bonds are often seen as one of the riskier inhabitants of a portfolio. However, recent stock market volatility tells a different story. The chart compares the Bank of America US High Yield Index with the S&P 500; it shows the market has dropped around 8.5% from 16 July to 5 August, while the US high yield universe actually lost less than 1%. Furthermore, high yield bonds have fully recovered, even reaching new highs for 2024.

There are technical reasons for high yield’s resilience but the point we are making here is related to the ‘defensive option’ embedded in high yield bonds. Just like any corporate bond, they can be decomposed in a risk-free yield and a risky credit spread. This latter component widened roughly 80-85 basis points but the total return effect was somewhat softened by the simultaneous sharp decline in US Treasury yields. Of course, we can compute a break-even between these two components but their inverse correlation is already a beneficial property for bond owners.

The other obvious benefit results from high yield’s rather contained duration, which is especially valuable during periods of relatively high absolute yield. The trade-off here is between credit risk and time value - investors enjoy an attractive carry profile, while at the same time avoid excessive sensitivity to spread widening. Once the US economy avoids recession – and we’re not forecasting one in the near future – investors should potentially reap the benefits.

Ecaterina Bigos, CIO Asia ex-Japan

China’s uphill journey of rebalancing its economy

China’s current economic armoury - infrastructure and manufacturing sector investment – appears to be helpful in defending its real GDP growth. However, it comes with a cost of entrenching deflationary pressures and rising concerns of overcapacity. The downward pressure on the Producer Price Index also affects export prices, which is contributing to the fears of exporting deflation. While this is being tolerated for now, as many countries grapple with high inflation, it could become problematic when inflation rates fall within target ranges.

An exit from deflation, helped by global trade, looks increasingly challenging. The rather notable sequential slowing in July’s exports, with broad-based easing across major developed and emerging markets, is sending tentative signals the export engine may soften. As the export sector has been an important growth driver for China’s economy in recent quarters, amid ongoing weakness in the housing sector and sluggish consumption growth, potential slowing would imply growing uncertainty on the industrial sector's growth outlook going into the second half of 2024.

This comes on the back of cautious signals from the external front of slowing demand. Further out, trade tensions concerns are a major uncertainty. The current stimulus plan, if fully implemented, without changes, may exacerbate the issue of overcapacity, add to disinflationary pressures, and increase the future debt burden.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

Rates | Developed economy data points to interest rate cuts from September - path from there is less certain. | |

|---|---|---|

US Treasuries | Fed likely to ease in September. Volatility remains a risk on new economic data and path from the first cut | |

Euro – Core Govt. | Further ECB rate cuts expected; political uncertainty remains a risk | |

Euro – Peripherals | Presents opportunities and higher real yields than Bunds | |

UK Gilts | Interest rate cuts fully discounted; markets await fiscal plans | |

JGBs | Uncertainty over Bank of Japan policy normalisation path. Yen remains volatile | |

Inflation | Stable expectations, with gradually lower inflation for the rest of 2024 |

Credit | Favourable pricing is increasing the asset class’s contribution to excess returns | |

|---|---|---|

USD Investment Grade | Without significant growth deterioration, credit to remain resilient | |

Euro Investment Grade | Resilient growth and lower interest rates support credit’s income appeal | |

GBP Investment Grade | Returns supported by better growth and expectations of rate cuts | |

USD High Yield | Narrative of growth without inflation is supportive. Fundamentals and funding remain strong | |

Euro High Yield | Strong fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Higher quality universe, well-placed with US interest rate cuts commencing |

Equities | Lower inflation will impact earnings cycle. Unmet return expectations from AI spending is a risk | |

|---|---|---|

US | Growth and quality to continue to dominate - but need to watch company earnings momentum | |

Europe | Attractive valuations, along with positive economic and earnings surprises | |

UK | Relatively more attractive valuations and positive economic momentum | |

Japan | Benefitting from semiconductor growth. Reforms and monetary policy in focus for broader performance | |

China | Growth remains unbalanced. Accelerating industrial output masks a weak consumer | |

Investment Themes* | Secular spending on technology and automation to support relative outperformance |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

CIO team views draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Disclaimer

AXA IM e BNP Paribas Asset Management stanno progressivamente fondendo e semplificando le loro entità legali per creare una struttura unificata. AXA Investment Managers è entrata a far parte del Gruppo BNP Paribas nel luglio 2025. A seguito della fusione di AXA Investment Managers Paris e BNP Paribas Asset Management Europe e delle rispettive holding, avvenuta il 31 dicembre 2025, le società combinate operano ora sotto il marchio BNP Paribas Asset Management Europe.

Prima dell’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate, si prega di consultare il Prospetto e il Documento contenente le informazioni chiave (KID). Tali documenti, che descrivono anche i diritti degli investitori, possono essere consultati - per i fondi commercializzati in Italia - in qualsiasi momento, gratuitamente, sul sito internet www.axa-im.it e possono essere ottenuti gratuitamente, su richiesta, presso la sede di BNP Paribas Asset Management. Il Prospetto è disponibile in lingua italiana e in lingua inglese. Il KID è disponibile nella lingua ufficiale locale del paese di distribuzione.

I contenuti pubblicati nel presente sito internet hanno finalità informativa e non vanno intesi come ricerca in materia di investimenti o analisi su strumenti finanziari ai sensi della Direttiva MiFID II (2014/65/UE), raccomandazione, offerta, anche fuori sede, o sollecitazione all’acquisto, alla sottoscrizione o alla vendita di strumenti finanziari o alla partecipazione a strategie commerciali da parte di BNP Paribas Asset Management o di società ad essa affiliate. L’investimento in qualsiasi fondo gestito o promosso da BNP Paribas Asset Management o dalle società ad essa affiliate è accettato soltanto se proveniente da investitori che siano in possesso dei requisiti richiesti ai sensi del prospetto informativo in vigore e della relativa documentazione di offerta.

Il presente sito contiene informazioni parziali e le stime, le previsioni e i pareri qui espressi possono essere interpretati soggettivamente. Le informazioni fornite all’interno del presente sito non tengono conto degli obiettivi d’investimento individuali, della situazione finanziaria o di particolari bisogni del singolo utente. Qualsiasi opinione espressa nel presente sito internet non è una dichiarazione di fatto e non costituisce una consulenza di investimento. Le previsioni, le proiezioni o gli obiettivi sono solo indicativi e non sono garantiti in alcun modo. I rendimenti passati non sono indicativi di quelli futuri. Il valore degli investimenti e il reddito da essi derivante possono variare, sia in aumento che in diminuzione, e gli investitori potrebbero non recuperare l’importo originariamente investito.

Ancorché BNP Paribas Asset Management impieghi ogni ragionevole sforzo per far sì che le informazioni contenute nel presente sito internet siano aggiornate ed accurate alla data di pubblicazione, non viene rilasciata alcuna garanzia in ordine all’accuratezza, affidabilità o completezza delle informazioni ivi fornite. BNP Paribas Asset Management declina espressamente ogni responsabilità in ordine ad eventuali perdite derivanti, direttamente od indirettamente, dall’utilizzo, in qualsiasi forma e per qualsiasi finalità, delle informazioni e dei dati presenti sul sito.

BNP Paribas Asset Management non è responsabile dell’accuratezza dei contenuti di altri siti internet eventualmente collegati a questo sito. L’esistenza di un collegamento ad un altro sito non implica approvazione da parte di BNP Paribas Asset Management delle informazioni ivi fornite. Il contenuto del presente sito, ivi inclusi i dati, le informazioni, i grafici, i documenti, le immagini, i loghi e il nome del dominio, è di proprietà esclusiva di BNP Paribas Asset Management e, salvo diversa specificazione, è coperto da copyright e protetto da ogni altra regolamentazione inerente alla proprietà intellettuale. In nessun caso è consentita la copia, riproduzione o diffusione delle informazioni contenute nel presente sito.

BNP Paribas Asset Management può decidere di porre fine alle disposizioni adottate per la commercializzazione dei suoi organismi di investimento collettivo in conformità a quanto previsto dall'articolo 93 bis della direttiva 2009/65/CE.

BNP Paribas Asset Management si riserva il diritto di aggiornare o rivedere il contenuto del presente sito internet senza preavviso.

Redatto da BNP Paribas Asset Management Europe. © BNP Paribas Asset Management 2026. Tutti i diritti riservati.